Techniques Of Finance Analysis

Finance Analysis Techniques

Financial analysis is the process of evaluating businesses, projects, budgets, and other finance-related transactions to determine their performance and suitability. Several techniques are employed to make informed investment and management decisions. These techniques can be broadly categorized into ratio analysis, trend analysis, cash flow analysis, and valuation analysis.

Ratio Analysis

Ratio analysis involves comparing different line items in a company's financial statements to derive meaningful insights. Key ratios include:

- Liquidity Ratios: These assess a company's ability to meet its short-term obligations. Examples include the current ratio (current assets / current liabilities) and the quick ratio (excluding inventory). A high ratio generally indicates good liquidity.

- Profitability Ratios: These measure a company's ability to generate profits relative to its revenue, assets, or equity. Examples include gross profit margin, net profit margin, return on assets (ROA), and return on equity (ROE). Higher ratios typically indicate better profitability.

- Solvency Ratios: These evaluate a company's ability to meet its long-term obligations. The debt-to-equity ratio and times interest earned ratio are common examples. Lower debt-to-equity and higher times interest earned ratios are generally favored.

- Efficiency Ratios: These measure how efficiently a company uses its assets to generate revenue. Examples include inventory turnover and accounts receivable turnover. Higher turnover ratios usually suggest better efficiency.

Trend Analysis

Trend analysis involves examining financial data over a period of time to identify patterns and predict future performance. This can be done using line graphs, bar charts, or regression analysis. Analyzing trends in revenue, expenses, and profits helps to understand the direction a company is heading and identify potential issues or opportunities. Common techniques include:

- Horizontal Analysis: Comparing financial statement items over time using percentage changes.

- Vertical Analysis: Expressing each line item in a financial statement as a percentage of a base item (e.g., expressing all income statement items as a percentage of sales).

Cash Flow Analysis

Cash flow analysis focuses on the movement of cash both into and out of a company. The statement of cash flows categorizes cash flows into operating, investing, and financing activities. Analyzing these cash flows helps to assess a company's ability to generate cash, fund its operations, and meet its obligations. Key metrics include:

- Free Cash Flow (FCF): The cash flow available to the company after paying for capital expenditures.

- Cash Flow from Operations (CFO): Cash generated from the company's core business activities.

Valuation Analysis

Valuation analysis aims to determine the intrinsic value of a company or asset. Several methods are used, including:

- Discounted Cash Flow (DCF) Analysis: Projecting future cash flows and discounting them back to their present value using a discount rate that reflects the risk of the investment.

- Relative Valuation: Comparing a company's valuation multiples (e.g., price-to-earnings ratio, price-to-book ratio) to those of its peers or industry averages.

- Asset-Based Valuation: Determining the value of a company based on the fair market value of its assets less its liabilities.

These financial analysis techniques are essential tools for investors, analysts, and managers to make informed decisions about investments, resource allocation, and overall financial performance.

800×457 technical analysis finance explained from tiblio.com

800×457 technical analysis finance explained from tiblio.com  925×750 financial analysis ratios profitability liquidity leverage from efinancemanagement.com

925×750 financial analysis ratios profitability liquidity leverage from efinancemanagement.com  500×350 financial analysis tools techniques from cajitintyagi.in

500×350 financial analysis tools techniques from cajitintyagi.in  180×233 financial analysis techniques ratios common size analysis from www.coursehero.com

180×233 financial analysis techniques ratios common size analysis from www.coursehero.com  810×1080 techniques financial analysis hobbies toys books magazines from www.carousell.sg

810×1080 techniques financial analysis hobbies toys books magazines from www.carousell.sg  1024×576 top techniques financial statement analysis analyst from imarticus.org

1024×576 top techniques financial statement analysis analyst from imarticus.org  1366×768 unveiling financial analysis techniques profi pioneers from profipioneers.com

1366×768 unveiling financial analysis techniques profi pioneers from profipioneers.com  591×626 premium vector financial analysis techniques accountants from www.freepik.com

591×626 premium vector financial analysis techniques accountants from www.freepik.com  1006×575 financial analysis techniques business school from esoftskills.com

1006×575 financial analysis techniques business school from esoftskills.com  2048×1152 financial analysis techniques from www.slideshare.net

2048×1152 financial analysis techniques from www.slideshare.net  1200×1535 financial analysis techniques financial analysis techniques elaine from www.studocu.com

1200×1535 financial analysis techniques financial analysis techniques elaine from www.studocu.com  1280×720 tools techniques measure tools techniques from www.slideteam.net

1280×720 tools techniques measure tools techniques from www.slideteam.net  950×489 financial analysis types techniquestools easy notes academy from easynotes4u.com

950×489 financial analysis types techniquestools easy notes academy from easynotes4u.com  2048×1448 major tools techniques financial statement analysis from studynotesexpert.com

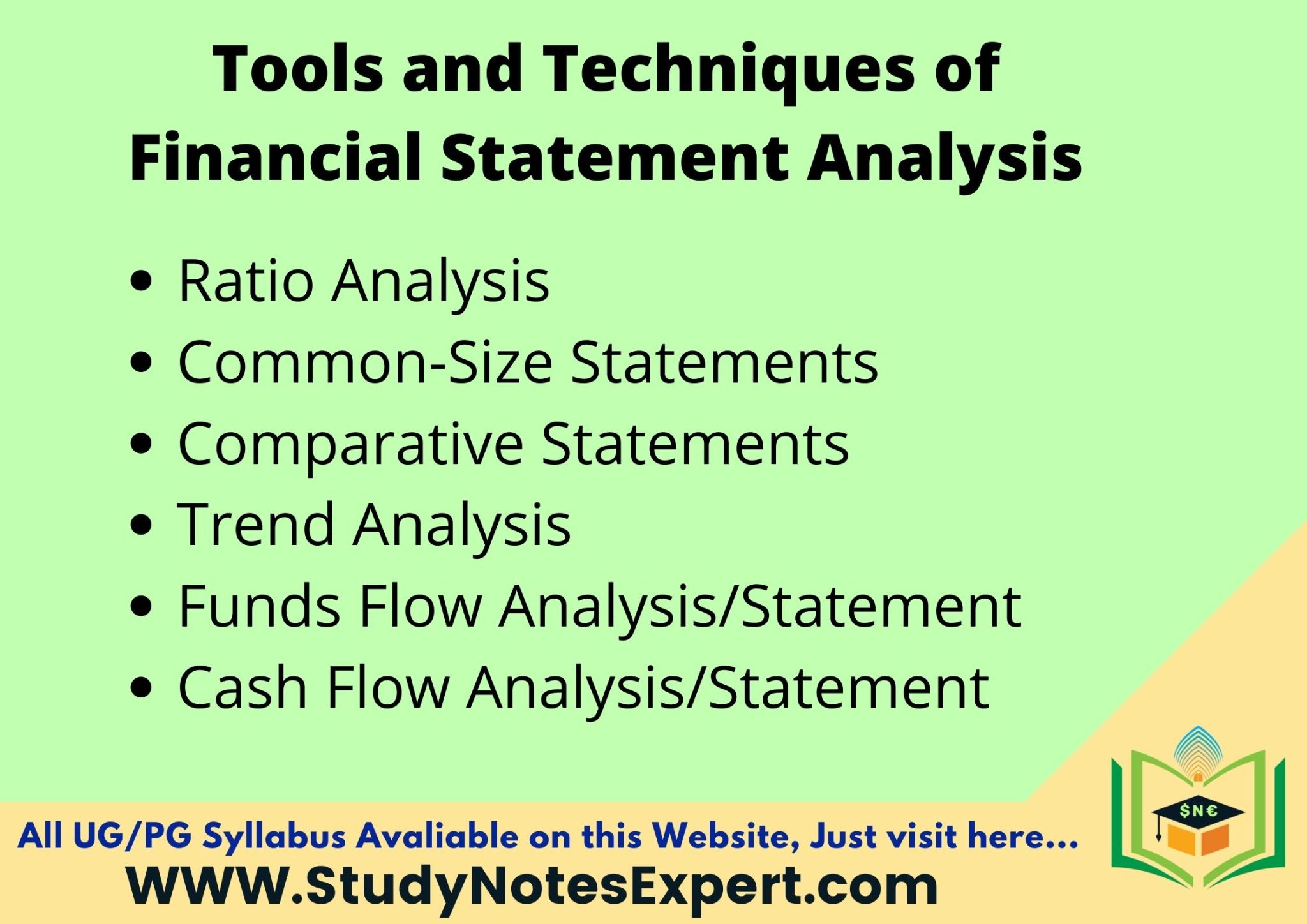

2048×1448 major tools techniques financial statement analysis from studynotesexpert.com  1280×720 financial statement analysis tools techniques tutors tips from tutorstips.com

1280×720 financial statement analysis tools techniques tutors tips from tutorstips.com  1620×911 solution financial analysis techniques studypool from www.studypool.com

1620×911 solution financial analysis techniques studypool from www.studypool.com  1833×907 process techniques financial statement analysis from enotesworld.com

1833×907 process techniques financial statement analysis from enotesworld.com  750×360 financial analysis types examples techniques analytics from www.analyticssteps.com

750×360 financial analysis types examples techniques analytics from www.analyticssteps.com  1620×2292 solution techniques financial statement analysis studypool from www.studypool.com

1620×2292 solution techniques financial statement analysis studypool from www.studypool.com  1200×675 top financial analysis techniques business analysts from www.computertechreviews.com

1200×675 top financial analysis techniques business analysts from www.computertechreviews.com  600×300 financial analysis techniques complete list techniques from oakbusinessconsultant.com

600×300 financial analysis techniques complete list techniques from oakbusinessconsultant.com  320×180 strategies techniques financial analysis from www.slideshare.net

320×180 strategies techniques financial analysis from www.slideshare.net  1620×2096 solution mastering financial analysis techniques business success from www.studypool.com

1620×2096 solution mastering financial analysis techniques business success from www.studypool.com  613×599 tools techniques financial statement analysis from www.tofler.in

613×599 tools techniques financial statement analysis from www.tofler.in  1200×1698 finance analysis finance analysis finance analysis important from www.studocu.com

1200×1698 finance analysis finance analysis finance analysis important from www.studocu.com  1200×1553 unit techniques financial analysis techniques financial from www.studocu.com

1200×1553 unit techniques financial analysis techniques financial from www.studocu.com  1280×720 methods approaches assess tools techniques from www.slidegeeks.com

1280×720 methods approaches assess tools techniques from www.slidegeeks.com  1200×1976 tools techniques financial analysis tools techniques from www.studocu.com

1200×1976 tools techniques financial analysis tools techniques from www.studocu.com  300×300 financial analysis meaning importance process limitations from commercemates.com

300×300 financial analysis meaning importance process limitations from commercemates.com