Finance Fixed Assets

Fixed assets, also known as property, plant, and equipment (PP&E), are long-term tangible assets a company owns and uses to generate revenue. Unlike inventory, which is sold to customers, fixed assets are held for use in production, providing services, renting to others, or for administrative purposes. Because of their long-term nature, they are not easily converted into cash and are expected to provide economic benefits for more than one accounting period.

Key Characteristics of Fixed Assets

- Tangible: They have a physical form, meaning you can touch and see them. Examples include land, buildings, machinery, vehicles, and furniture.

- Long-Term: They are held for use over an extended period, typically longer than one year. This distinguishes them from current assets like cash or accounts receivable.

- Used in Operations: They are employed in the company's day-to-day activities to produce goods or services, and are not intended for resale.

- Subject to Depreciation (Except Land): With the exception of land, most fixed assets wear out or become obsolete over time. This decline in value is recognized as depreciation expense on the income statement.

Examples of Fixed Assets

The specific fixed assets a company owns will depend on the nature of its business. Common examples include:

- Land: Used for building sites, farmland, or other business purposes.

- Buildings: Factories, offices, warehouses, and retail stores.

- Machinery and Equipment: Used in manufacturing, production, or providing services.

- Vehicles: Cars, trucks, and other transportation equipment.

- Furniture and Fixtures: Office furniture, display cases, and other interior assets.

- Computer Equipment: Servers, computers, and other IT infrastructure.

Accounting for Fixed Assets

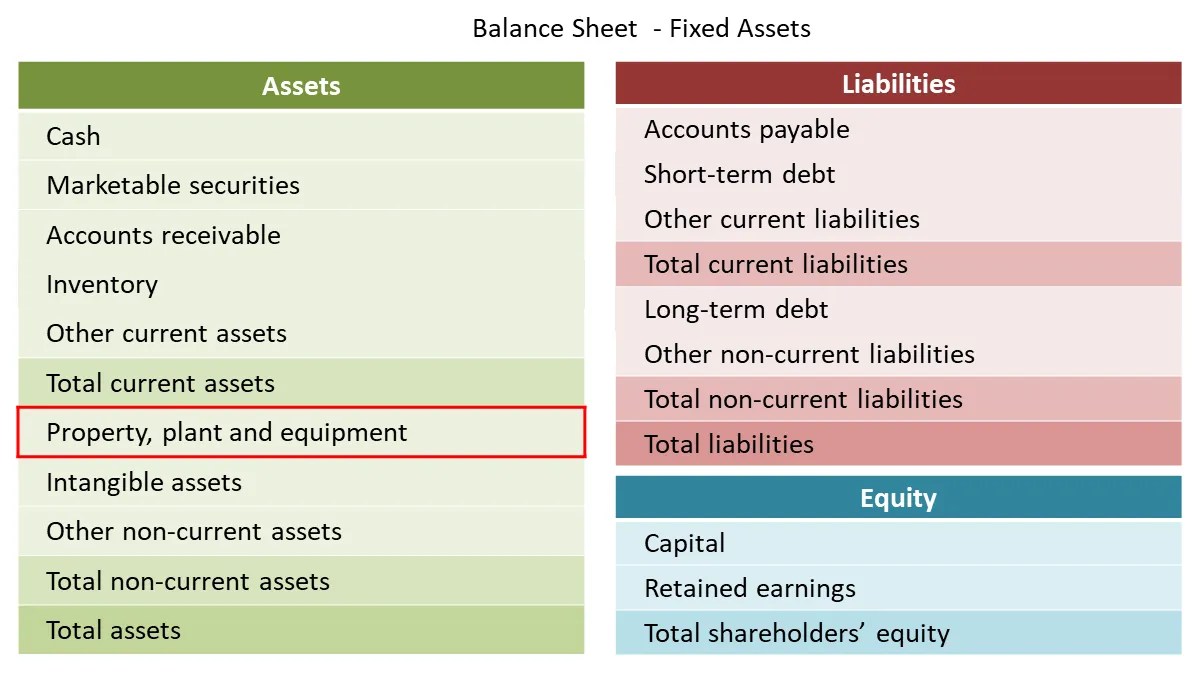

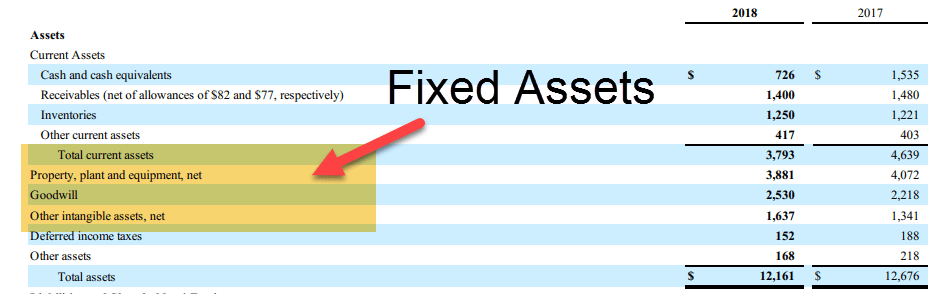

Fixed assets are initially recorded on the balance sheet at their historical cost, which includes the purchase price plus any costs incurred to get the asset ready for its intended use (e.g., installation costs, transportation fees). Over time, these assets (except land) are depreciated. Common depreciation methods include:

- Straight-Line: Allocates an equal amount of depreciation expense each year.

- Declining Balance: Applies a higher depreciation expense in the early years of an asset's life and a lower expense in later years.

- Units of Production: Bases depreciation expense on the actual usage or output of the asset.

The accumulated depreciation is recorded in a contra-asset account, reducing the carrying value (book value) of the fixed asset on the balance sheet. When a fixed asset is sold or disposed of, the company recognizes a gain or loss equal to the difference between the proceeds from the sale and the asset's carrying value.

Importance of Managing Fixed Assets

Effective management of fixed assets is crucial for a company's financial health. This includes:

- Tracking and Maintenance: Ensuring assets are properly maintained to extend their useful life and prevent costly repairs.

- Capital Budgeting: Carefully evaluating potential fixed asset investments to ensure they generate a positive return for the company.

- Depreciation Planning: Selecting the appropriate depreciation method to accurately reflect the asset's decline in value.

- Disposal Strategies: Developing strategies for efficiently disposing of assets when they are no longer needed.

By properly managing their fixed assets, companies can optimize their operational efficiency, improve their profitability, and maintain accurate financial records.

768×617 fixed asset wordpress from docs.axolonerp.com

768×617 fixed asset wordpress from docs.axolonerp.com  768×543 fixed assets financial learning class from financiallearningclass.com

768×543 fixed assets financial learning class from financiallearningclass.com  1200×675 fixed assets from fity.club

1200×675 fixed assets from fity.club  1280×720 fixed assets balance sheet accouting formula fixed assets from www.educba.com

1280×720 fixed assets balance sheet accouting formula fixed assets from www.educba.com  960×413 fixed asset definition examples bookstime from www.bookstime.com

960×413 fixed asset definition examples bookstime from www.bookstime.com :max_bytes(150000):strip_icc()/fixedasset-edit-3fa5166c806b4897921df1a7dbcb5826.jpg) 1500×1000 fixed assets net fixed assets formula calculation from fity.club

1500×1000 fixed assets net fixed assets formula calculation from fity.club  900×500 fixed assets difference fixed assets current assets from www.educba.com

900×500 fixed assets difference fixed assets current assets from www.educba.com  1740×2044 fixed assets examples lists business fields careercliff from www.careercliff.com

1740×2044 fixed assets examples lists business fields careercliff from www.careercliff.com  412×399 fixed assets management impact consulting from impactconsultingng.com

412×399 fixed assets management impact consulting from impactconsultingng.com  1024×768 fixed assets powerpoint id from www.slideserve.com

1024×768 fixed assets powerpoint id from www.slideserve.com  500×382 fixed assets accountingcapital from www.accountingcapital.com

500×382 fixed assets accountingcapital from www.accountingcapital.com  1066×840 nbk fixed assets finance from www.nbk.com

1066×840 nbk fixed assets finance from www.nbk.com  2000×1333 fixed assets erp solution bahrain gcc countries from www.erpoptimum.com

2000×1333 fixed assets erp solution bahrain gcc countries from www.erpoptimum.com  1000×700 fixed assets definition types characteristics examples from happay.com

1000×700 fixed assets definition types characteristics examples from happay.com  1024×576 understanding fixed assets fogwingio from www.fogwing.io

1024×576 understanding fixed assets fogwingio from www.fogwing.io  1120×630 understanding importance fixed assets business mdh from www.mdh.me.uk

1120×630 understanding importance fixed assets business mdh from www.mdh.me.uk  936×526 fixed assets godlan from godlan.com

936×526 fixed assets godlan from godlan.com  942×294 fixed assets types list examples advantages from www.wallstreetmojo.com

942×294 fixed assets types list examples advantages from www.wallstreetmojo.com  1896×860 fixed asset accounting examples hourly from www.hourly.io

1896×860 fixed asset accounting examples hourly from www.hourly.io  1165×552 fixed assets reporting analysis technology from 5ytechnology.com

1165×552 fixed assets reporting analysis technology from 5ytechnology.com  1081×1081 fixed assets current assets understanding differences from www.tagsamurai.com

1081×1081 fixed assets current assets understanding differences from www.tagsamurai.com  1200×630 fixed assets accounting shiksha from www.shiksha.com

1200×630 fixed assets accounting shiksha from www.shiksha.com