Ytc Finance Formula

```html

YTC Finance, often referring to Yield-to-Call (YTC), is a crucial metric for bond investors. It represents the total return anticipated on a callable bond if that bond is held until its first call date. Understanding YTC is vital because callable bonds can be redeemed by the issuer before their maturity date, impacting the investor's potential gains.

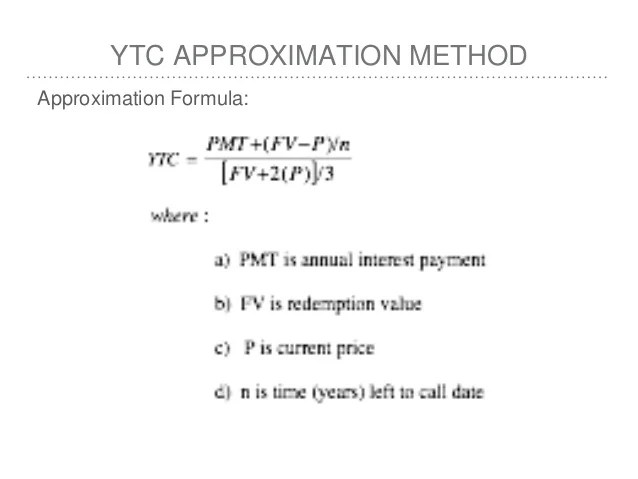

The YTC formula is more complex than the simpler Yield-to-Maturity (YTM) formula. It considers the possibility of the bond being called back, effectively shortening the investment horizon. This calculation accounts for the difference between the bond's current market price and its call price, along with the coupon payments expected until the call date.

Here's a simplified breakdown of the YTC formula:

YTC ≈ (C + (CP - MP) / N) / ((CP + MP) / 2)

Where:

- C = Annual Coupon Payment

- CP = Call Price (Price at which the bond can be redeemed)

- MP = Current Market Price of the bond

- N = Number of years until the first call date

Let's illustrate with an example. Imagine a bond with a face value of $1,000, an annual coupon rate of 5% (so C = $50), a current market price of $950 (MP), and a call price of $1,010 (CP) that can be exercised in 3 years (N). Plugging these values into the formula:

YTC ≈ ($50 + ($1010 - $950) / 3) / (($1010 + $950) / 2)

YTC ≈ ($50 + $20) / ($980)

YTC ≈ $70 / $980

YTC ≈ 0.0714 or 7.14%

Therefore, the approximate Yield-to-Call for this bond is 7.14%. This represents the annualized return an investor can expect if the bond is purchased at $950 and held until the issuer calls it back at $1,010 in 3 years.

Several factors influence YTC. Changes in interest rates are a primary driver. As interest rates rise, the value of existing bonds generally falls, potentially increasing the YTC for callable bonds as they trade at a discount to their call price. Conversely, falling interest rates can make callable bonds more attractive to issuers, increasing the likelihood of them being called and potentially decreasing the YTC for investors who purchased the bond at a premium.

It is important to remember that the YTC is an estimated figure. The actual return may vary depending on whether the bond is actually called and the reinvestment rates available for the coupon payments received. Furthermore, the formula provided is an approximation. More precise calculations may involve iterative methods or financial calculators to account for the time value of money accurately.

In summary, Yield-to-Call is a valuable tool for evaluating callable bonds, offering investors insight into their potential returns, particularly in environments where interest rate volatility and call risk are significant concerns. Always consider consulting a financial professional before making investment decisions.

```

181×233 ytc formula calculator step step ytc formula from www.coursehero.com

181×233 ytc formula calculator step step ytc formula from www.coursehero.com  768×430 ytc calculator from calculatorshub.net

768×430 ytc calculator from calculatorshub.net  1259×713 ytc price action trading joshuamartinezorg from joshuamartinez.org

1259×713 ytc price action trading joshuamartinezorg from joshuamartinez.org  535×227 yield maturity ytm approximation formula from financetrain.com

535×227 yield maturity ytm approximation formula from financetrain.com  1200×1553 ytm ytc ytc yield call years from www.studocu.com

1200×1553 ytm ytc ytc yield call years from www.studocu.com  600×291 yield call ytc definition formulas calculate from kylonews.com

600×291 yield call ytc definition formulas calculate from kylonews.com  680×418 yield maturity ytm yield call ytc from www.bbalectures.com

680×418 yield maturity ytm yield call ytc from www.bbalectures.com  700×372 solved hw calculate ytc financial calculator cheggcom from www.chegg.com

700×372 solved hw calculate ytc financial calculator cheggcom from www.chegg.com  650×321 yfinance python package spreadsheet row from rowzero.io

650×321 yfinance python package spreadsheet row from rowzero.io  1500×1000 yfinance tutorial stock prices andriy blokhin from andriyblokhin.com

1500×1000 yfinance tutorial stock prices andriy blokhin from andriyblokhin.com  474×197 perpetual bond formula kerrinsigurd from kerrinsigurd.blogspot.com

474×197 perpetual bond formula kerrinsigurd from kerrinsigurd.blogspot.com  723×374 yield call meaning formula efm from efinancemanagement.com

723×374 yield call meaning formula efm from efinancemanagement.com  1796×498 yfinance library definitive guide qmr from www.qmr.ai

1796×498 yfinance library definitive guide qmr from www.qmr.ai  600×315 yield maturity ytm assignment point from www.assignmentpoint.com

600×315 yield maturity ytm assignment point from www.assignmentpoint.com  1600×1000 loi suat thu hoi yield call ytc la gi from vietnambiz.vn

1600×1000 loi suat thu hoi yield call ytc la gi from vietnambiz.vn  821×458 fixed income formula find ytm step from quant.stackexchange.com

821×458 fixed income formula find ytm step from quant.stackexchange.com  638×479 ytm ytc approximationbasic finance bsba copy from www.slideshare.net

638×479 ytm ytc approximationbasic finance bsba copy from www.slideshare.net